Do We Need Glass-Steagall for the Combination Pizza Hut and Taco Bell?

A reply to Anna Stansbury and Larry Summers on their concentration and investment paper from last year.

In one of the most poorly timed debuts for a major paper, Declining Worker Power and American Economic Performance (NBER), by Anna Stansbury and Larry Summers, first came out on March 18th, 2020, the week lockdowns started across the country. I read it and had a lot of thoughts, which I immediately outlined in a Google Doc before getting back to writing about what would become the CARES Act. My goal was to get back to the outline when things calmed down, and that never really happened. But today I just got my second vaccine shot (Team Pfizer), and thought it would be good to celebrate that by finishing the thing I had last wanted to write before the pandemic took over our lives.

It definitely deserves attention, in addition to the coverage it is already receiving (VoxEU, Marginal Revolution, Edsall). I’ll start by saying that I love the conclusion, something that needs to be heard more:

“The monopsony and monopoly perspectives suggest that the rise in inequality has come alongside the economy becoming less efficient, which allows economists to be in the congenial place of arguing for policies that simultaneously perfect markets, increase efficiency and promote fairness.

[But] if declines in worker power have been major causes of increases in inequality and lack of progress in labor incomes, if policymakers wish to reverse these trends, and if these problems cannot be addressed by making markets more competitive, it raises questions about capitalist institutions. In particular, it raises issues about the effects of corporate governance arrangements which promote the interests of shareholders only [...]

And it suggests that institutions which share rents with workers are likely to be necessary as a form of countervailing power (of the sort initially proposed by Galbraith (1952)).”

I think this is exactly right, and it is one reason I and others sometimes get uncomfortable with the way “competition” is deployed within discussions about inequality, as if a perfectly competitive market is either a realistic goal or a desirable objective for society. I wrote a book about how we need freedom from markets in more spheres of our lives, not fewer.

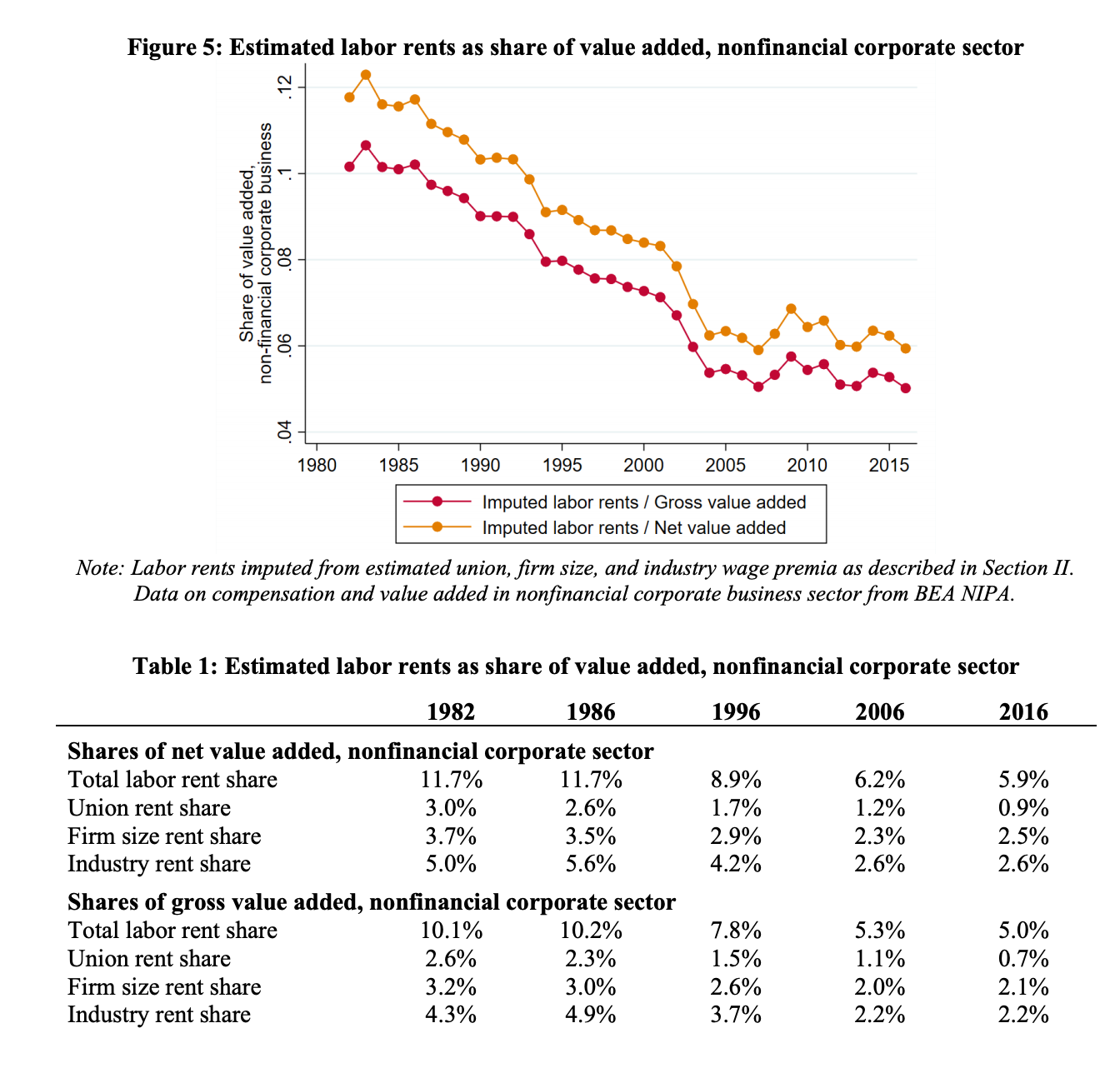

There’s a lot to the paper, which creates an index of labor market rents, centered around unionization, returns to firm size, and industry-specific rents, and shows how they’ve each declined over the past forty years. They also show how the decline of labor market rents can explain many aggregate economic questions. Two of their arguments are worth unpacking: that (1) concentration can’t explain stagnating wages for workers, which I agree with. But also (2) that weakened labor power, rather than an explosion of corporate power, explains the corporate stagnation we see of weak investments, high profits, and large markups. I have questions about this second argument.

Concentration and Wages

The Stansbury/Summers paper is partially a reaction against claims that increasing concentration of employers is a driver of wage stagnation over the past 40 years. This is taking the term monopsony literally, as if a fewer number of employers in an area are the reason bosses have increased power over workers and their wages. This argument has been pushed by the new wave of antitrust scholars, and as often happens in advocacy there was a strong effort by the advocates to make their issue of concentration central to the larger debate about wages.

You’ve probably heard a lot about increased concentration in recent years, so you might be surprised that the claim that it has driven wage stagnation is very controversial within left-liberal scholarship. This paper adds evidence to the argument, notably in Bivens, Mishel, and Schmitt (2018) and Rinz (2018), that concentration among businesses as local employers has not increased significantly since the late 1970s, and it may not have increased at all. (Though industries are definitely becoming more concentrated at the national level [Grullon et al], it doesn’t have to follow that areas have more concentrated employers.) And no matter how you specify it, concentration of employers hasn’t increased at the levels that would motivate the major shifts in labor incomes that took place since the 1980s.

I never cared for this “employer concentration drives monopsony and low wages” argument. I think the essential part of the monopsony literature is that exploitation and unequal bargaining is built into the labor contract itself. Focusing on concentration reifies a “competitive market” as the solution and the goal in itself for the labor market, as opposed to something that doesn’t exist and would annihilate human and social life if it did exist. As the excellent work by the Unequal Power project at the Economics Policy Institute shows, this assumption that we just need the background conditions for fair competition to have a just labor market has disastrous impacts and is unfortunately woven into the fabric of law, philosophy, and economic thinking.

I find it important that the original research on minimum wage and employer monopsony power focused on fast-food employment. Fast-food employers don’t gain their monopsony power from concentration. They aren’t like the auto industry having 80 percent of the employment in Flint, Michigan during the 1930s; delicious as they would be, there are no Combination Pizza Hut and Taco Bell company towns. Fast-food employers’ market power derives from the insecurity present in poverty wages, the difficulty in searching for new jobs, an overall depressed economic environment, the need to secure wages to survive, and other features of capitalism. Putting a Glass-Steagall legal separation at the Combination Pizza Hut and Taco Bell - lest their market domination in the supply of fantastic cheese sauces allows them to corner the employment of both nachos workers and stuffed crust pizza workers - would do nothing to fight their market power over employees. The problem is the labor contract itself.

Though this was an ugly fight in 2018, it’s more or less mellowed out since then with a “yes, and” cease-fire. There’s probably concentration monopsony at this moment in time; notably Stansbury, in other academic work as well as a policy-relevant summary, finds employer concentration can play a role in the cross-section of wages, stating “we find that moving from the 75th to the 95th percentile of employer concentration (across workers) reduces wages by 5%.” But not the time-series of wages; this probably doesn’t play any major role in the vast increase in inequality over the past forty years. Labor market concentration should play a role in merger guidelines, but we should also focus on unions and minimum wages, even if that takes us away from the chimera of a “competitive market.” You can see the balance in Zach Carter’s discussion of economist Joan Robinson, which notes “that workers, as sellers of their own labor, almost always faced monopsonistic exploitation from employers, the buyers of their labor” but also that “corporate concentration has suppressed worker wages over the past quarter-century.” It’s a balance.

Weak Corporate Investment as Disguised Wage Stagnation?

The second point of the Stansbury/Summers paper is trying to downplay research that, in my mind, best explains the current state of our economy. This research mostly starts with an iteration of this graphic (taken from Gutiérrez/Philippon 2017):

Here you can see corporate profits skyrocketing while investment doesn’t increase at anywhere near the same rate. If you were to take these as a ratio of investments over profits, you’d see it fairly flat until about 2000, at which point it collapses. This is also a period in which interest rates are declining, so the cost of financing investment is falling. These conditions shouldn’t exist at the same time in a market economy; firms should take advantage of easy financing to invest more and drive down excess profits.

This body of work has expanded in many directions. One great summary of the arguments around how firms have higher markups and that measures like Tobin’s Q have exploded can be found here at (Eggertsson, Robbins, and Getz Wold 2018). Work by (Barkai 2020) argues that both labor and capital shares have fallen, the latter the result of falling interest rates, and instead we need to be discussing and measuring an excess “profit share” instead. Others debate whether intangible assets are actually closing the investment gap; still others argue we should see this as the result of “superstar firms” out-producing other firms (Autor et al 2020, but see also Gutiérrez and Philippon 2019 for a critical response). It’s a very productive conversation.

In Stansbury and Summers’ paper, workers used to receive a significant labor rent premium. This premium from unionization, size and industry has fallen, and it’s not just the result of shifts within industries. So far, so good. Stansbury and Summers go further and argue that what the above literature is describing is essentially a redistribution in the firm; that the relationship between total profits and investments are relatively consistent if you include labor rents in addition to total profits. So instead of seeing a corporate stagnation problem, what we are really seeing is an accounting illusion where decreasing labor rents add to excess profits while nothing much else has changed. Or as they also find, “we analyze our measures of labor power alongside three measures of profitability at the industry level over 1987-2016 [...] suggesting again that the decline in worker power has more explanatory power than the rise in concentration for changes in industry-level profitability.”

Three things that jump out at me.

1 - Timing and Periodization.

First is that I think a better periodization of the analysis is needed. The things we worry about in the corporate stagnation literature really take off starting in 2000. Above is their measure of labor rents. Their measure looks like it bottoms out by 2004, with the major fall having occurred by 2000. This timeline is consistent with other labor market indicators; notably the growth of interfirm inequality and the decline of unionization. Yet, their results put the entire period from 1987 to 2016 in the equation.

When I think of the story of our unequal economy, I tend to break into two periods: 1980 to 2000 and 2000 until now. The first is the period of labor stagnation, the second is where corporate stagnation takes off. One can look at the Barkai “profit share” below, or the break in the ratio of profits and investment above, or even versions of the fall of labor share, to see these as things that take off only after the labor rents have been driven down. They don’t move at the same time, but sequentially.

I think the literature itself is moving in this direction. For instance, there’s been a body of work that argues mergers in particular become worse after 2000. Consider a study whose thesis is right in the title, “From Good to Bad Concentration? U.S. Industries over the past 30 years” by Covarrubias, Gutiérrez, and Philippon. They find: “During the 1990’s, and at low levels of initial concentration, we find evidence of efficient concentration driven by tougher price competition, intangible investment, and increasing productivity of leaders. After 2000, however, the evidence suggests inefficient concentration, decreasing competition and increasing barriers to entry, as leaders become more entrenched and concentration is associated with lower investment, higher prices and lower productivity growth.” That’s directly in line with this periodization.

So I’d like to see how sensitive the investment results are to taking both these time periods as one.

2 - Rent measure as exogenous to corporate structure?

(This point probably made more sense when I wrote the outline down a year ago, out of respect for history I’m going to try and trace my idea.) Their regression looks at concentration versus labor rents. Yet while concentration is a metric of industry conditions and an input into bargaining, things like the firm size premiums are a consequence of the bargaining process. For instance, if increasing shareholder power (the thing I think explains many of these dynamics) over production was driving both the reduction in the large firm premium and also an increase in profits through less competition, one might see the former drive the second using this metric. One thing I’m curious about (and it may be in a later version or appendix, there’s a lot of materials) is what unionization alone tells us, as that is at least a partially exogenous variable driven by law. But right now, reading the paper, I’m still a little lost on how I should understand how to understand the two types of variables and stories - labor versus corporate - in the regressions.

3 - Competition.

The paper argues that a decline in labor power could result in a higher level of profit but a consistent amount of investment, thus explaining the rise of corporate stagnation. But why wouldn’t this increase the level of competition? To simplify, a firm makes $100 with an investment. Before it would split it with labor, so $50 to labor and $50 to capital and profits. Now it’s $90 to capital and $10 to labor. This would, for example, increase Tobin’s Q because it increases profits but not investment. This is basically the story of the paper in relation to the FRED graphic above - “while net investment over net operating surplus (profits to capital) has fallen substantially over the last thirty years in the nonfinancial corporate sector, average net investment over our measure of net total profits has only declined very slightly.” Below you can see their graphic where the investment over profits ratio doesn’t fall if you add labor rents to the profits.

But why wouldn’t this fall of labor rents increase competition and investment? The presumption is that the decline in labor power is an economy-wide event. So the decline in rents to labor also would happen for new competitors as well. This increased $90 to capital should make competition more appealing since new entrants can also only pay the $10 rent to labor. So competition on the capital side should increase to drive down Tobin’s Q, which is to say that I’m not sure why an industry-level fall in labor share would not increase investment. I know there’s a model they provide, but I still find it confusing on the second read. This would need a more straightforward story associated with it for me to buy.

All that said, this is a great paper and contribution. It’s important we’re discussing the corporate sector again as an actual thing, as opposed to the abstracted, ethereal bundle of potential competition that exists in the world of law-and-economics and our legal system. Here’s hoping to continue that work, and bring it into real-world application soon.