Rethinking the Biden Era Economic Debate

A critical response to Jason Furman's "Post-Neoliberal Delusion and the Tragedy of Bidenomics," that dives into both the administration and ideas of the past 4 years.

I believe one reason there’s been a conservative vibes shift was that the recent Democratic loss was broad enough to hit any theory of what the Democratic Party coalition should look like and what their agenda should be going forward. So there’s going to be some necessary autopsies of what went wrong; but they’ll also need to be refined through pushback. Jason Furman, whose work I have learned tremendously from, has a recent indictment of the Biden administration, The Post-Neoliberal Delusion and the Tragedy of Bidenomics, in Foreign Affairs, The Biden administration is guilty of “discarding conventional economic considerations of budget constraints, tradeoffs, and cost-benefit analysis” as a result of “giving in to the post-neoliberal delusion.”

Others have written responses to Furman, and I’d highly recommend Jared Bernstein on how Biden’s economics team saw things, Noah Smith for how Biden tackled genuinely new problems for which we need better answers, and Chris Hughes on the necessary shift in economic policymaking. I’m sure there will be more from people better equipped to answer this indictment. But I want to add some specifics first on the administration and second on the question of economic ideas. My takeaway is that what the Biden administration was trying to do was an evolution of policymaking in dialogue with changing evidence and challenges, something the popular coverage has really missed.

An Administration in Hindsight

I think we shouldn’t confuse “you disagreed with me” for “you didn’t consider tradeoffs.” To take the central indictment and the one I know best, the passage of the American Rescue Plan (ARP), tradeoffs and cost-benefit structured the entire debate. I agree with Furman that “economic ideas also played an important role” in the passage of the American Rescue Plan, but not the ones he mentioned. They were ideas within the mainstream based on the best economic evidence available at the time.

The case for going bigger was that the risks of hitting the ‘zero lower bound,’ or ending up in a situation where the economy remains stuck for a long time, means that the penalty for going too low is asymmetrically larger. The idea that the United States had trended, due to global savings, the aging of the population, and inequality and concentration towards a state where the economy was more prone to this downward stuckness - generally called ‘secular stagnation’ - was widespread going into the pandemic and changes the risk matrix.

Meanwhile, on the costs side, between 1991 and 2019, unemployment had ranged from 3.5% to 10% with essentially no change in inflation, leaving experts understanding the relationship between demand and inflation to be essentially “flat.” During the first Trump term, unemployment got to that 3.5%, way below what economists had said possible. And prime-age labor force participation also increased, which experts spent the mid 2010s saying would not happen. In addition, the economy absorbed the fiscal shock of Trump’s Tax Cuts and Jobs Act. All of these happened without any inflationary consequences, and all pointed at the time to the risks of going too big to be muted.

Indeed, in the chart above of Blue Chip forecasts of inflation and interest rates in April 2021, following the passage of the American Rescue Plan (and as auto inflation started to already pick up), even the very highest estimates completely missed the mark of where inflation would go.

I bring this up not to say the ARP was the correct size or that the political motivations that drove the Plinko-style legislative process machine final law were correct.1 I say this only to note that these debates were not separated from the leading economic arguments of their time. Now we may have broken out of secular stagnation, with the neutral rate rising, and new ideas and arguments will be needed.

Obviously inflation dominated the economic politics of the era and overshadowed everything else. But I don’t agree with Furman’s argument that the “new economic philosophy that dominated during the Biden years emphasized demand over supply.” Secretary Yellen and others built a whole sincere case around “modern supply-side economics,” the investments and infrastructure laws that were passed clearly were meant to boost supply over the subsequent decade, and the case for investments in care labor were, in part, driven by labor force supply. (Indeed, universal pre-K is probably the best active labor market policy we have available.)

And also obviously the failure to pass major social spending through Build Back Better was a failure. But I disagree with Furman's implication, following one op-ed, that the Biden team thought their investments “would transform the economy such that more traditional Democratic social policies would become unnecessary.” But as NEC Deputy Director Bharat Ramamurti emphasized recently, the choice matrix was actually quite small in the Senate, blocked by Senator Manchin’s aversion to cash programs and Senator Sinema’s to higher new taxes. In that case, there’s a good expected-value case to be made for going all-in on the fully refundable tax credit, rather than go for a still unlikely and less effective program.

There’s also a little of having it both ways. After implying that the Biden administration didn’t care about redistribution, Furman quickly notes the expansion of the premium tax credits for the Affordable Care Act (ACA) health care exchanges. And, as noted in the graphic above, President Biden was able to add something like 10 million people to the ACA marketplaces, an odd accomplishment for an administration indifferent to redistribution. The continuity here is actually important to flag. In an August 2016 JAMA medical article, President Obama outlined the three next steps for expanding the ACA: (1) “Congressional action to increase financial assistance to purchase coverage,” (2) “a public plan to compete alongside private insurers in areas of the country where competition is limited,” (3) “give the federal government the authority to negotiate prices for certain high-priced drugs.”

Between the ARP and the Inflation Reduction Act, the Biden administration got the first of these from 2021 to 2025, and the third permanently for Medicare. Senate political limitations no doubt blocked a permanent expansion of the first and excluded the second. There are also things that are less splashy but important, whether it’s the (sadly not covered well enough) Summer EBT program to expanding and updating SNAP, whose existence shows that this was a priority.

It’s a general interest and non-technical magazine, but I don’t follow the argument that the administration didn’t take crowding out seriously in their industrial policy, and as such that made the Biden investments largely net ineffectual. (That Bernstein and Smith are also confused by this gives me comfort that I'm not alone.) According to a recent Biden-era Treasury’s analysis, private investment exceeds historical trends by over $400 billion dollars and high returns to capital and record new business formation all point more to crowding-in than crowding-out.

Did Post-Neoliberals Hijack Everything and Not Understand Tradeoffs?

But there’s a second set of arguments embedded in this that economic policymaking was hijacked by a “post-neoliberal delusion” whose ideas are counter to sound economic policymaking. I don’t use the term neoliberal/post-neoliberal if I can avoid it; the general way I would describe the moment is that the economic ideas animating a generation of policymakers couldn’t answer the challenges of the 21st century, and new ideas and priorities need to be developed. But I do have four responses to the argument as presented here.

First, a serious problem with discussing economic ideas is that they change in ways that you immediately forget. So, as an example, a Democratic Council of Economic Advisors (CEA) chair in the 1990s would have understood that shooting down the idea of increasing the minimum wage was an essential part of the job. Out here in 2025, former CEA chair Jason Furman criticizes the Biden administration for not increasing it in this article. Part of that reflects new empirical evidence informing new ideas of how labor markets work, that pervasive search frictions mean monopsony power over workers is prevalent even in competitive markets. But we go from A to B here and immediately forget we were ever on an intellectual journey.

Second, and I think this is just a problem of the coverage and the way it is sourced that I should write about one day, the change in ideas is treated as some kind of break or “conquering” rather than evolution in face of new evidence and new challenges. Most people in the Biden administration were also in the Obama administration. But even by the end of the Obama administration economic ideas were changing; would we have had President Biden’s executive order on competition without Furman’s work on increased consolidation and market power at the CEA? That work, not an argument you’d make in the mid-1990s (if only because concentration hadn’t picked up yet), helped open the gates for more people to study, research, innovate, and explore questions about how to address the challenge of market power. Furman might not like where it ended up, but it iteratively built on the things he and others had started.

Indeed most of the best sourced reporting on the Biden administration policymakers, whether it’s Bruce Reed on antitrust or Janet Yellen on trade with China, put it exactly into this evolutionary frame, where people had one set of opinions in the 1990s and evolved them to face the challenges as they stand out here in the 2010s-2020s. One noteworthy person here is Gary Gensler, who was criticized by progressives when hired by the Obama administration but turned out to be a strong implementer of the Dodd-Frank Act and an aggressive financial regulator under Biden, much to the chagrin of crypto-embracing Democratic “popularists.” (Indeed financial reform is another thing that went from A to B between the 1990s and 2010s yet that epic journey just goes unnoticed now.) Gensler, who went from Goldman Sachs to a Robert Rubin protégé to a strong financial reformer shows that the conquering metaphor needs work. Who is going to put Reed, Yellen, and Gensler in a room and yell at them for having no clue about 1990s policymaking?

Third, there is something funny about calling for more analysis at a moment when conventional wisdom is moving to see these kinds of impact and economic analyses as delaying actions or mere pretexts for lawsuits in the context of stopping action and supply (which they certainly were for Dodd-Frank). But Furman is wrong that post-neoliberal types don’t take cost-benefit seriously. In fact, in terms of actually thinking through the frontier of what economic and cost-benefit analysis looks like, they have been leading the charge.

Furman himself has brought this up in a roundabout way. In his September 2024 talk on tradeoffs, a likely precursor to this piece, Furman notes that many economic tools aren’t doing a good enough job and need to be made better (my bold):

“But the analysis done in the government and by outside groups is often not do enough to help inform policymakers [...] Government agencies calculate total costs and benefits without considering the effects of these policies on marginal utility which will differ because of their distributional impact (although I should note, that in principle President Biden’s recent Executive Order includes these considerations).”

There’s a lot of people who contributed to being able to incorporate distributional impact, including head of OIRA Richard Revesz, but a very notable one is law professor (and a co-founder of the post-neoliberal related Law and Political Economy Project) Sabeel Rahman, who helped shepherd it through the process as a lawyer at OIRA. Here’s Rahman discussing the benefits of Circular A4 revision he and others fought for at the Law and Political Economy website. Other scholars pushed back, but that there was a debate showed that this world takes these issues quite seriously.

Among other changes, the ways in which traditional Kaldor-Hicks efficiency in cost-benefit analysis can amplify inequality were explored in an important 2018 piece by economist Zachary Liscow who criticized traditional cost-benefit analysis in a law review article (and who would have supervised the equivalent circular for investments in Circular A94 while at OMB).2 While sounding technical, and it is, it goes to the very foundational question of how costs and benefits are understood in economic policymaking.

Many of the exaggerated tradeoff assumptions that informed a generation of policymaking - that inequality generates growth, that weakening unions and employee protections will lead to a more dynamic labor market, that competitive markets and the financial sector will take care of themselves if left alone, that markets eliminate discrimination - stopped seeming to answer the basic questions of the economy during the 2010s. That doesn’t give people carte blanche to just make stuff up or to ignore having to empirically and theoretically ground one’s analysis. But there are new problems we face, and old ideas need to be updated.

My old boss, Andy Rich, who studied think tanks, once described (paraphrasing) that policy advocacy was like playing Plinko; you can help decide where the thing starts at the top (in particular, by making the case for prioritization and answering objections), but the final landing place is going to involve a level of politics that is so out of your control it might as well be random.

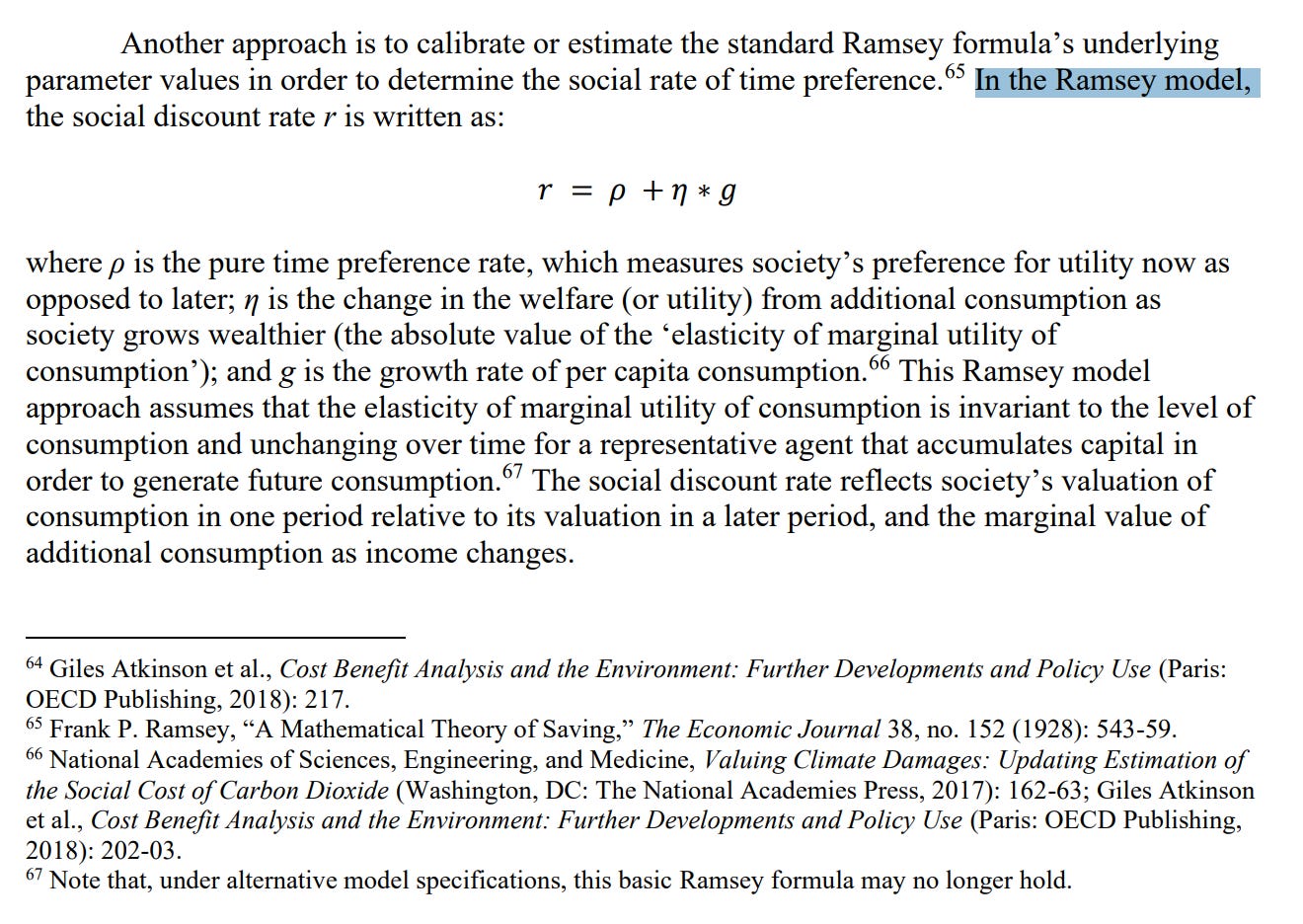

My favorite piece was that as originally proposed circular A4 allowed the Ramsey model to be used in long-term cost-benefit analysis, at a moment when the intergenerational nature of current actions matters:

But that didn’t survive to the final rule. Oh what could have been! Note Democrats terrorizing bureaucrats with more homework and more complicated algebra around discounting is much better than the current terror campaign ripping through the government.

This is all so dumb—we hemorrhaged manufacturing jobs to China from 2002-2009 in the aftermath of China into the WTO!! From 2005-2008 CPI was significantly elevated peaking at 5.6% in July 2008 because of high energy prices due to the commodity super cycle what was led by China!! The Global Financial Crisis happened in that context!! The GFC happened because lower class disposable income was being degraded by inflation while the China Shock was undermining the job market!! Neoliberalism failed!! WTF is Furman even talking about??

Search fractions do not cause monopsony power in labor markets (though job heterogeneity might). Every search model that has monopsony power in it generates it by assuming 1) perfectly inelastic demand at firm level, 2) fixing the number of firms in the market, effectively shutting off the two margins of adjustment. It's assuming perfectly inelastic labor demand, not search frictions.