The Federal Reserve vs. the Tariff Shock: What If It Isn’t Transitory?

As global supply chains fray and the economy veers towards recession, the Federal Reserve faces a different spin on a recent problem — one it can’t fully fix.

Summary:

As Trump’s tariffs hit the real economy, a reasonable estimate is that unemployment rises by 1 percentage point—possibly 2—meaning a loss of between 1.7 and 3.4 million jobs.

The Fed will aim to protect inflation expectations—and there’s already evidence those expectations are starting to shift.

The COVID supply shock was a one-time shift in the price level; tariffs at this magnitude could create a one-time shift in the inflation rate.

It’s not just the stock market. Trump’s tariffs will tear through the real economy, and the Federal Reserve’s ability to respond will be limited due to how these supply shocks affect inflation. To understand this, let’s compare today’s situation to 2021-2023. This is speculative, but let me explain my thinking.

First, the basics: the announced tariffs are significantly higher than financial markets anticipated two weeks ago. The House likely can’t achieve the two-thirds majority needed to override President Trump’s veto of legislation reasserting congressional control over tariffs, and courts won’t act fast enough to prevent damage. As a result, growth forecasts are declining.

By how much? Goldman Sachs revised their 2025 real GDP growth forecast from 2.4% to 0.5%. The Yale Budget Lab has a -1.1% impact on real GDP from the tariffs alone. Forecasters have generally estimated that GDP in 2025, previously estimated around 2%, will come to a halt, but are divided on whether it goes negative to cause a recession. I want to stick with a 2 percentage point drop.

Is a 2 percentage point drop plausible? Yes. It’s the largest tax increase since the 1960s and it falls regressively on lower incomes, dragging growth downward. Current trade disruptions will create confusion, shutdowns, and delays, boosting inflation and reducing real incomes. Additionally, unprecedented policy uncertainty, greater even than during COVID, will delay investments. Financial markets are signaling slowdowns and even political risk, with the abnormal event of rising interest rates alongside a falling dollar.

What does that mean for everyday people? In general, a 2% drop in real GDP raises unemployment by about 1 percentage point—taking it to approximately 5.2%. That means 1.7 million jobs are lost.

How should we think of the range around this estimate? On one hand, the economy was fine when President Trump inherited it. There aren’t real problems driving this downturn further into a recession. Yet historically, as Goldman Sachs researchers have noted, unemployment rarely increases by just 1%. Even the mildest past recession raised unemployment by 1.9%.

When unemployment rises, it usually continues. The Biden administration successfully reversed the Sahm Rule, which briefly crossed 0.5% last summer and has historically triggered a recession. But that scenario depended on unique conditions around a ‘soft landing’ and statistical anomalies from a brief low-unemployment period. We can’t count on that now; a 2% unemployment increase remains plausible.

However, everyone is flying blind. The FRB/US model the Federal Reserve uses doesn’t have a trade war default option, because this kind of crude mercantilism at this scale would have been a waste of time to try and program. FRB/US aggregates imports and exports into single price measures, insufficient to capture complex supply-chain risks. Research shows such networks are both more productive and more vulnerable than typically recognized.

So What Does the Fed Do?

Everyone expects the Fed to cut interest rates. Tariff-induced inflation will be viewed as a one-time supply shock, similar to European VAT shifts, echoing the "transitory" inflation debates of 2021-2023 when inflation declined without a severe recession or high unemployment.

Yet, this situation differs significantly.

Bernanke on Supply Shocks

Wait, wasn’t the transitory stuff disproven? No. Here’s former Federal Reserve Chair, chairman of George W. Bush Council of Economic Advisers, and Nobel Prize winner Ben Bernanke at the January 2025 American Economics Association (full video), making the case that this was, in fact, driven by the supply side, and not demand:

Watch the full clip, but a key quote:

I think the inflation was caused, pretty much, by the supply side. […] there were some folks, I won’t mention any names, saying that getting inflation down was going to cost a lot of unemployment […] those of us who thought this was a supply-side shock said, ‘no, it’ll be a pretty benign disinflation.’ As the supply shocks unwind, we’d expect decent strong growth.

When it was time to compile people who argued the post-pandemic inflation was supply-driven, it was fun that the go-to list was this former W. Bush official, the head of Lazard, and the research teams at JP Morgan and Goldman Sachs.1 And I believe they are all right. The output sacrifice ratio for 2022-2024 has the wrong sign; you don’t get 4.5 percentage points of disinflation with extra growth without something moving on the supply side.

(I think there’s actually a soft economics conventional wisdom that the inflation was mostly supply-side, but it’s not breaking into the political conventional wisdom as that’s being filtered by people with big feelings about the Biden administration, intra-Democratic Party coalitional fighting, people who felt burnt by how long and broad this major cost-push shock was, and economists who want to use it as part of the case to leave the wilderness.)

Insurance Against a Persistent Shock

However, the Federal Reserve took rates into restrictive territory. Why? I found the best explanation from Federal Reserve economist Jeremy Rudd (and author of the excellent A Practical Guide to Macroeconomics), back in March of 2023 (video, at 1h18m). I’m going to quote at length, because it’s good to hear how this is understood at the Fed:

This is just me talking: [the Federal Reserve is] basically trying to prevent something like the 1970s from occurring again. In other words, right now inflation's underlying stochastic trend appears incredibly invariant to any kind of economic developments.

Whereas in the 1970s, and the 1980s through maybe the mid-1990s, inflation responded a lot to economic conditions, [such as] past inflation or the level of slack in the economy. And what we're trying to do is to keep that from happening. And that's a great thing. Because if you don't have to worry about inflation's stochastic trend moving, if you don't have to worry about inflation becoming unanchored from some sort of long-run level, then you can make policy a lot more easily. You can see through a lot of shocks, you can push harder for full employment, and you don't have to worry about the implications.

So what we're doing basically is saying: okay, we want to keep that situation from happening. We're taking out insurance to do so. But that's not really what's being said. What's being said is: we're trying to keep inflation from being entrenched because for some reason that's going to be bad for workers. Well, the worst thing for workers is losing their job. [...]

What we're doing by trying to lean against inflation as aggressively as we are, is saying: we're taking out insurance because the last thing we want is to go back to a situation like the accelerationist Phillips curve or of the 1970s and 1980s, the kind of thing where price increases fit through the wages fed through different price increases in a very persistent way. That would be a terrible outcome.

We don't know how that outcome occurred to bring us to this happier situation where that doesn't seem to happen. But we want to take out some insurance to ensure that it doesn't.

2021-2023 inflation was a cost-push shock, but raising interest rates into restrictive territory was an insurance policy. It served two purposes: first, it was protection in case the Federal Reserve was incorrect about inflation’s primary drivers. More important, it guarded against the possibility that, even if the Fed correctly identified a cost-push shock, this shock might embed itself into inflation expectations and thus persistently elevate nominal spending and inflation.

It’s true that inflation depends less on economic conditions since 1991. As Figure 2 shows, the Phillips Curve became more “flat,” even for PCE core non-housing services. The comment above reminds me there’s a positive here too, that maintaining this helps pursue full employment. But note this cuts both ways - unemployment going up this year is unlikely to reduce inflation enough to offset tariff effects.

This scenario makes a clear argument for why the Fed might maintain or even tighten rates further. There's a real risk inflation could become unanchored from its longer-term underlying trend, either due to shifting expectations or other unforeseen factors.

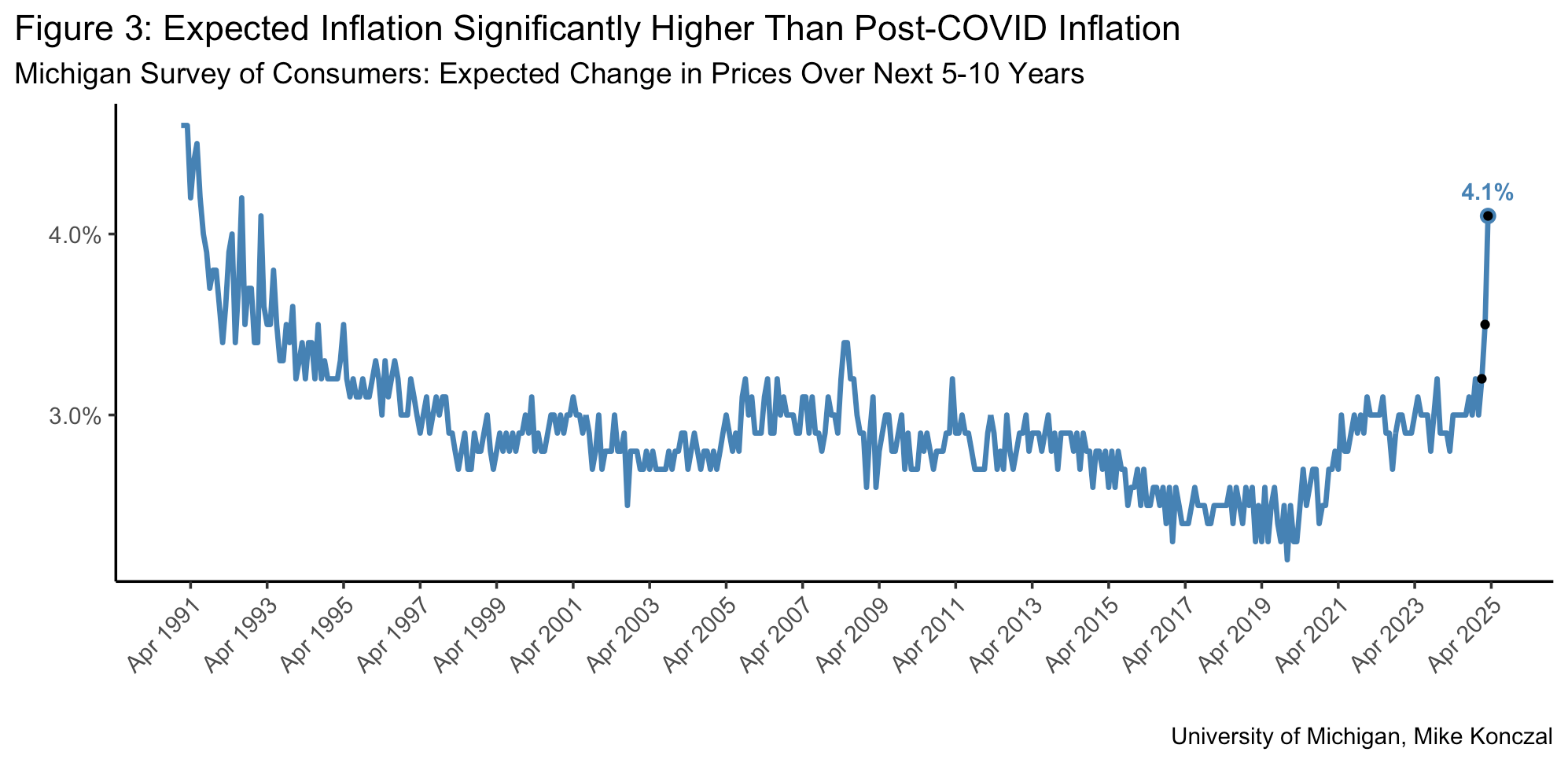

And right on cue, recent data from the University of Michigan Consumer Sentiment report underscores these risks, and the numbers do not look encouraging:

Frankly, this is shocking. This never happened during the 2021–2023 inflation, or even under Trump’s first-term tariffs. During the reopening inflation, the Fed made it clear they’d cause a recession to stop inflation, President Biden made it clear he respected their independence to fight inflation, and longer-term expected inflation never picked up.

But another key question arises: what exactly is the nature of this shock?

Are We Ever Going to Be ‘So Back’?

Let’s approach it narratively first: during the 2021-2022 inflation wave we didn’t forget how to make things. The lockdowns and reopening made it so we didn’t have enough inputs to make the quantities we needed. But once that was over - once the ports were cleared, and there were enough semiconductors, and businesses adjusted to the shifts in spending and labor conditions - we’d be back. Here’s Chair Powell on 60 Minutes in February 2024, describing why we didn’t need a recession to bring down inflation:

POWELL: But I'll tell you why I think it is. And that is that it was these pandemic-related distortions, both of demand and supply. [...]

So with demand, we had people spending money so much on goods and not so much on services. [...] So, there's a shortage. So, what happened is inflation just spiked. But as the semiconductor supply came back, prices, the inflation has moderated a great deal. So really, these unique features of the pandemic did reverse in a way that brought inflation down.

(This is him saying “cost-push” without saying it.) Or as Joe Stiglitz described in February 2022, “We know how to make cars and chips as well today as we did two years ago.”

But what if we now don’t actually know how to make cars and chips as well as we did two years ago? What if the supply shock is permanent, not temporary? Typically, tariffs haven’t create such persistent shocks. However, broad global tariffs imposed on a highly interconnected world could effectively reset decades of integrated supply chains, creating a much longer-lasting disruption to contrast against the chaotic but ultimately transient shocks seen during the reopening in 2021 or the land war in Europe in 2022.

A Toy Model for Intuition

To clarify our intuitions further, let's explore this through a quick simulation. We'll use a straightforward three-equation New Keynesian model, incorporating backward-looking inflation expectations, from economists Wendy Carlin and David Soskice (2005), which really should replace the static intermediate macroeconomic approach.

There’s three main equations we need. (1) Spending in the economy is influenced by interest rates.2 (2) Inflation is the result of demand being above aggregate supply, cost-push shocks, and expected inflation. (3) The central bank sets interest rates to balance between inflation and output. You can check this footnote for more details.3

This isn’t calibrated to anything, the numbers are arbitrary, I just want this exercise to flesh out intuitions. Let's first simulate a temporary cost-push shock that eventually reverses. In Scenario 1 on the left, the Fed actively offsets the shock. In Scenario 2, the Fed decides to "look through" the shock, keeping rates unchanged.

Following, you can see the supply shock in the top line. In the first scenario, you see the Fed raise rates (A) and cause a recession (B). In the other scenario, the Fed not adjusting interest rates leads to a one-time shift in the price level (C)(remember these are rates), while output remains stable.

Again, this is not calibrated, but Treasury estimates at the tail-end of the Biden administration thought you’d need unemployment to hit about 10% to 14% - above the Global Financial Crisis! - to keep the pre-pandemic price level on track.

Now, consider a one-time reversed and permanent supply shock scenario, with the Fed looking through both:

Instead of reversing, it’s a one-time hit to the supply level (E). We really did forget how to make things. And here, the permanent shock doesn't simply shift the inflation level; it shifts the inflation rate (F), continuously pushing prices higher over time. This persistent inflationary pressure is precisely what the Federal Reserve is determined to prevent.

I don’t think this is the base case for the tariff shock. But it is a possibility. And I do not envy how the Federal Reserve has to balance this problem this year.

Before all this, I would relax by YouTubing Cubs at Game 7 of the 2016 World Series White Sox at Game 4 of the 2005 World Series, Jordan's shrug at the 1992 Finals, or anything from the 1985 Bears. But now it’s all about grilling a large steak, pouring an oversized Negroni, and listening to this September 2022 Goldman Sachs podcast where Olivier Blanchard and Goldman’s Jan Hatzius debate whether the Beveridge Curve means we need a recession to have disinflation - Jan said nope, and crushed it.

All the inflation fighting is over the second, Phillips Curve, aggregate supply equation. Greedflation! Nonlinearity! Cost-push shocks! Deviations from natural job openings rate! But to me the thing most intellectually stressed by this recovery is the demand equation. The idea that the Federal Reserve uses restrictive rates to defer aggregate consumption and investment seems far-fetched given gangbuster spending. But the idea that the Federal Reserve affects demand by causing financial crises and putting brutal Stiglitz-style credit rationing on new innovative businesses and the most vulnerable tracks. Or, as James Tobin said in 1980 against using monetary policy for stabilization, “monetary restriction” either pushes on a string or is “pushed hard enough to produce a credit crunch that reverses the economy's direction [which] acts quickly but severely."

Here are the relevant equations and here is the Github where the model (refactoring of this) lives in R code:

Code for downloading and making graphics in this post is here.

One cannot trust the bogus inflation numbers produced by the government that continue to be "understated."

Great post.

Not exactly central to the point here, but: what do you make of the argument that the level shift in trend NGDP growth implies that demand played a meaningful role in 2021-2023? I find it compelling but maybe that’s because I don’t really understand basic NK dynamics.